TL;DR

- Le rapport sur l’emploi non agricole a surpris les marchés, atténuant les inquiétudes relatives à une récession, tandis que la hausse du taux de chômage renforce les attentes d’une baisse des taux.

- Les données attendues cette semaine incluent les indices Fed de Chicago, Dallas et Richmond, la seconde estimation du PIB américain T3, le PCE cœur d’octobre, etc.

- Correction marquée du marché : BTC a chuté de 7,88 %, ETH de 9,44 %, et les ETF BTC et ETH affichent de fortes sorties hebdomadaires (–1,22 Md$ et –500,25 M$).

- Le contexte macroéconomique reste fragile : MicroStrategy pourrait être retirée des indices, l’indice Fear & Greed demeure à 19 (Extrême peur), et le ratio ETH/BTC glisse à 0,326.

- Les altcoins sont particulièrement touchés, la capitalisation totale crypto ayant diminué de 7,48 %. Hors actifs majeurs, le recul atteint 5,89 %, tandis que les actifs hors du top 10 chutent de 9,18 %.

- Top 30 : baisse moyenne de -9,8 %. Seuls BCH (+12,8 %), WLFI (+7,6 %) et LEO progressent. BCH bondit grâce à des positions longues de baleines ; WLFI progresse malgré une faille de sécurité et une destruction d’urgence de 22,14 M$. HYPE -14,7 % après un déblocage de 320 M$.

- La Fondation Ethereum dévoile Interop Layer pour résoudre la fragmentation L2 et l’interopérabilité.

- Aave Labs lance une application d’épargne à haut rendement avec dépôts assurés et prise en charge de 12 000 banques.

- Paxos lance USDG0 pour favoriser la liquidité réglementée du dollar entre chaînes.

Vue d’ensemble macro

Le rapport sur l’emploi non agricole a surpris les marchés, atténuant les inquiétudes relatives à une récession, tandis que la hausse du taux de chômage renforce les attentes d’une baisse des taux

En septembre, les États-Unis ont créé 119 000 emplois non agricoles, dépassant le consensus de 51 000, tandis que les chiffres des deux mois précédents ont été révisés à la baisse de 34 000. Le taux de chômage a augmenté de 0,1 point à 4,4 %, légèrement au-dessus des attentes. La croissance du salaire horaire moyen a reculé de 0,2 point à 0,2 % en rythme mensuel, en dessous des 0,3 % prévus. La durée moyenne hebdomadaire reste stable à 34,2 heures, conformément aux prévisions. Ce dynamisme de l’emploi atténue les inquiétudes du marché. Parallèlement, la hausse du chômage et la modération des salaires renforcent les attentes d’une baisse des taux par la Fed.

Malgré des taux toujours restrictifs, qui laissent une marge à la Fed pour agir, les signes de reprise et les dissensions internes réduisent la probabilité d’une baisse en décembre. La présidente de la Fed de Boston, Susan Collins, n’a pas encore arrêté sa position, tandis que le président de la Fed de New York, John Williams, estime possible une baisse du taux directeur. Le Bureau of Labor Statistics (BLS) publiera ensemble les chiffres d’octobre et novembre le 16 décembre ; le rapport de septembre est donc la dernière statistique officielle à disposition de la Fed avant la prochaine réunion du FOMC. L’attention se porte aussi sur les premières demandes d’allocations chômage et autres indicateurs liés aux licenciements et au shutdown gouvernemental.

Les données attendues cette semaine incluent les indices Fed de Chicago, Dallas et Richmond, la seconde estimation du PIB américain T3, le PCE cœur d’octobre, etc. En raison de Thanksgiving, la semaine sera raccourcie, mais verra la publication décalée des prix à la production US et des enquêtes des Fed régionales, ainsi que la confiance des consommateurs Conference Board. Les autres statistiques seront publiées progressivement, les perturbations liées au shutdown continuant d’affecter la diffusion officielle. (1, 2)

Polymarket : Décision de la Fed en décembre

DXY

Le dollar américain s’est maintenu au-dessus de 100 depuis lundi dernier, proche d’un plus haut de six mois, alors que les investisseurs évaluent les orientations de la Fed et que les divisions entre gouverneurs régionaux s’affirment. (3)

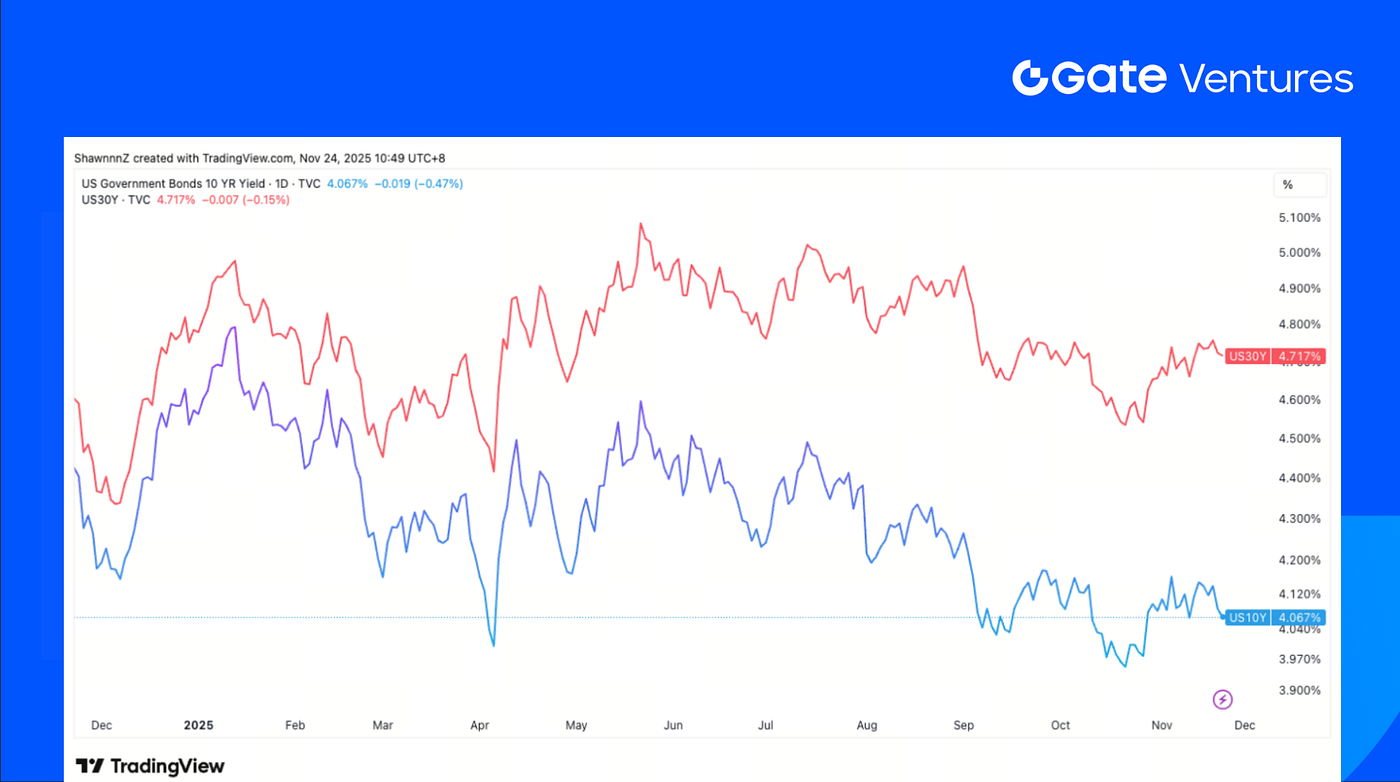

Rendements US 10 ans et 30 ans

Les taux obligataires US à court et long terme ont reculé vendredi, après que le président de la Fed de New York a déclaré entrevoir « une marge d’ajustement supplémentaire à court terme dans la fourchette cible ». (4)

Or

Le prix de l’or est resté stable la semaine passée, les investisseurs renforçant leurs paris sur une baisse des taux en décembre après le signal accommodant du président de la Fed de New York. (5)

Vue d’ensemble des marchés crypto

1. Principaux actifs

Prix du BTC

Prix de l’ETH

Ratio ETH/BTC

BTC a perdu 7,88 % sur la semaine, ETH 9,44 %, prolongeant la dynamique baissière. Les ETF BTC enregistrent quatre semaines consécutives de sorties nettes (–1,22 Md$ cette semaine) ; les ETF ETH restent faibles avec –500,25 M$ de sorties hebdomadaires. (6)

MicroStrategy pourrait être retirée des indices MSCI et Nasdaq, ses actifs numériques représentant désormais plus de 50 % de l’ensemble de ses actifs, avec un coût moyen du BTC à 74 430 $, ce qui pèse sur le sentiment général. (7)

L’indice Fear & Greed demeure à 19, dans la zone « Extrême peur », et le ratio ETH/BTC poursuit son repli de 1,77 % à 0,326, signalant la sous-performance d’ETH. (8)

2. Capitalisation totale du marché

Capitalisation totale crypto

Capitalisation totale hors BTC et ETH

Capitalisation hors top 10

La capitalisation totale du marché crypto a reculé de 7,48 % la semaine passée. Hors BTC et ETH, le marché élargi perd 5,89 %, tandis que les actifs hors du top 10 enregistrent une forte baisse de 9,18 %. Les altcoins ont donc subi une correction plus forte que les actifs majeurs.

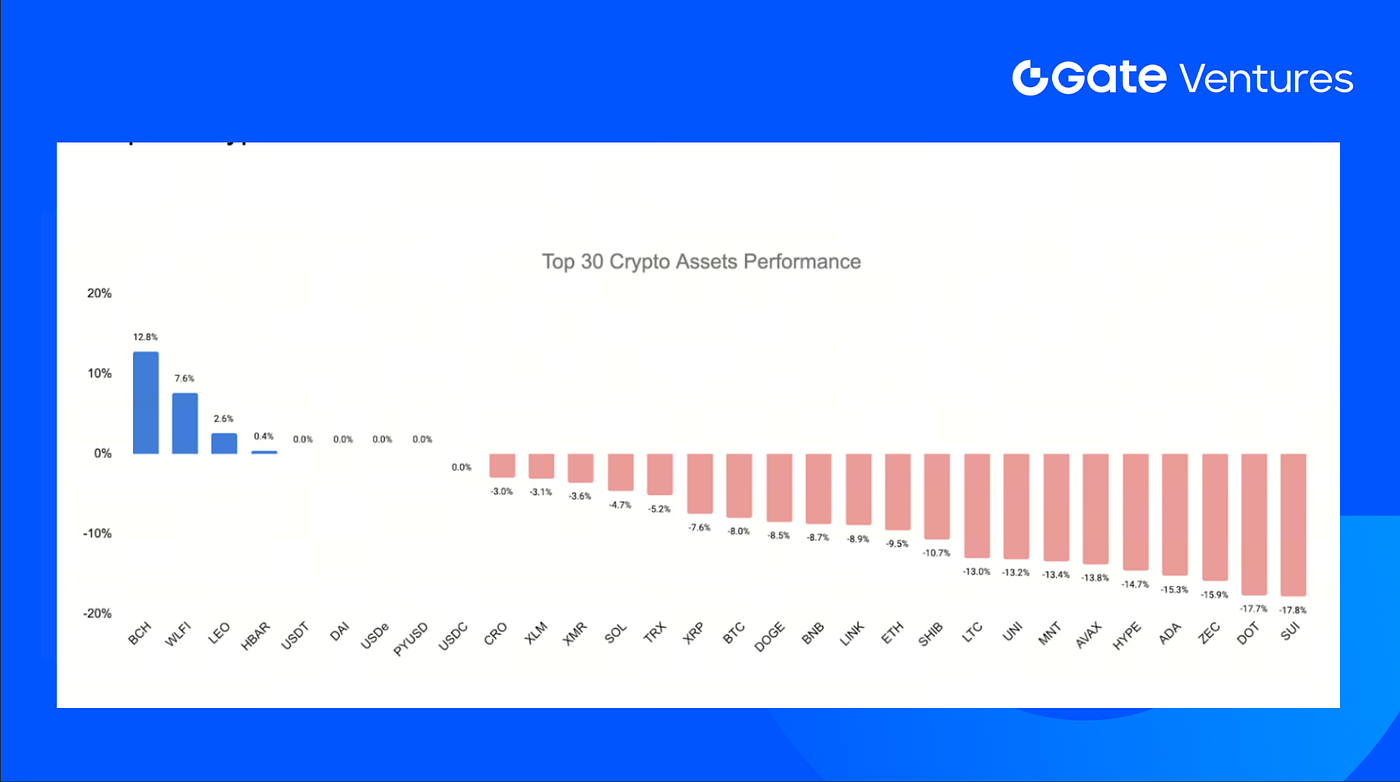

3. Performance des 30 principaux actifs crypto

Source : Coinmarketcap et Gate Ventures, au 24 novembre 2025

Parmi les 30 principaux actifs crypto, les prix ont reculé en moyenne de 9,8 % sur la semaine. Seuls BCH, WLFI et LEO affichent des gains.

BCH se distingue avec une hausse de 12,8 %, portée par une activité de baleines sur Hyperliquid, où de gros traders ont pris des positions longues 10x sur BCH pour près de 900 000 $. (9)

WLFI progresse de 7,6 %, bien qu’un incident de sécurité majeur ait été annoncé, impactant des portefeuilles utilisateurs avant le lancement officiel. L’équipe a gelé les portefeuilles concernés et réalisé une destruction urgente de tokens pour 22,14 M$. (10)

Côté baisse, HYPE recule de 14,7 % après un déblocage de 320 M$, générant une forte pression vendeuse. (11)

Faits marquants du secteur crypto

1. La Fondation Ethereum dévoile Interop Layer pour résoudre la fragmentation L2 et l’interopérabilité

La Fondation Ethereum a présenté de nouveaux détails sur son Interop Layer, un protocole sur chaîne conçu pour éliminer la fragmentation de l’écosystème L2 en forte croissance. S’appuyant sur l’abstraction de compte ERC-4337, l’Interop Layer rend les portefeuilles et dapps nativement multichaîne, permettant les transferts et interactions sur tous les rollups sans passerelles ni UX spécifiques. Désormais ouvert aux tests, ce dispositif renforce la stratégie de scalabilité d’Ethereum en unifiant la liquidité, en améliorant l’expérience développeur et en restituant une expérience chaîne unique à l’environnement EVM. (12)

2. Aave Labs lance une application d’épargne à haut rendement avec dépôts assurés et prise en charge de 12 000 banques

Aave Labs lance une application d’épargne proposant un taux de base de 5 %, jusqu’à 9 % avec des primes d’activité, et une protection assurantielle sur les dépôts jusqu’à 1 M$. Le produit connecte plus de 12 000 banques et cartes de débit pour le financement fiat, tout en permettant des transferts illimités de stablecoins. Les rendements DeFi sont ainsi proposés comme alternative sécurisée et accessible aux comptes d’épargne fintech. Les intérêts proviennent des marchés surcollatéralisés d’Aave, où Aave Labs capte l’écart entre les taux utilisateurs et le rendement du protocole sous-jacent. L’application sera lancée sur iOS, avec une liste d’attente désormais ouverte. (13)

3. Paxos lance USDG0 pour favoriser la liquidité réglementée du dollar entre chaînes

Paxos Labs a présenté USDG0, extension omnichaîne de son stablecoin réglementé USDG, permettant le déplacement d’une réserve unique, entièrement adossée, sur Hyperliquid, Plume et Aptos via le standard OFT de LayerZero. La solution évite les actifs enveloppés et conserve les garanties réglementaires et le rendement indexé sur le Trésor. Chaque écosystème peut intégrer USDG0 dans le trading, le lending ou les infrastructures DeFi, aboutissant à une liquidité homogène sans recours aux passerelles traditionnelles. Ce lancement étend le Global Dollar Network, alors que Paxos poursuit la montée en puissance de la tokenisation réglementée, avec plus de 180 Md$ traités depuis 2018. (14)

Principaux deals Ventures

1. 0xbow lève 3,5 M$ en Seed round sur fond de demande croissante pour des infrastructures de confidentialité réglementées

0xbow a levé 3,5 M$ en Seed round mené par Starbloom Capital, avec Coinbase Ventures, BOOST VC et d’autres investisseurs, pour développer Privacy Pools, protocole conforme lié à l’initiative Kohaku de la Fondation Ethereum. S’appuyant sur les recherches initiées par Vitalik Buterin, le système permet l’anonymisation des fonds tout en filtrant les acteurs malveillants. Ce financement soutient les extensions multi-actifs et le déploiement inter-chaînes, consolidant la position de 0xbow comme infrastructure de confidentialité alignée sur les exigences réglementaires. (15)

2. Une équipe d’anciens de BlackRock lève 4,6 M$ pour HelloTrade — infrastructure d’abord sur mobile de trading d’actifs américains

HelloTrade a levé 4,6 M$ auprès de Dragonfly Capital, Mirana Ventures et d’autres, pour sa plateforme blockchain d’accès global aux actifs américains. Fondée par d’anciens responsables digital-assets de BlackRock, la solution vise à simplifier la participation transfrontalière aux actions et matières premières via une interface d’abord sur mobile. Les fonds soutiennent le lancement, la sécurité et l’éducation utilisateur, positionnant HelloTrade comme infrastructure innovante pour l’accès retail aux marchés traditionnels via des canaux sur chaîne. (16)

3. Ledn reçoit un investissement stratégique de Tether pour développer le prêt sur collatéral BTC

Ledn a reçu un investissement stratégique de Tether pour étendre sa plateforme de prêts garantis par bitcoin, après avoir octroyé plus de 2,8 Md$ de crédits et dépassé les 100 M$ d’ARR. Les fonds soutiennent les infrastructures de conservation, de gestion du risque et de liquidation, à mesure que le prêt BTC-collatéralisé centralisé s’étend auprès des particuliers et institutionnels. Ce dispositif permet aux emprunteurs de débloquer de la liquidité sans vendre leur BTC, répondant à la demande croissante de crédit non dilutif et positionnant Ledn comme infrastructure clé pour la prochaine génération de services financiers bitcoin. (17)

Metrics marché Ventures

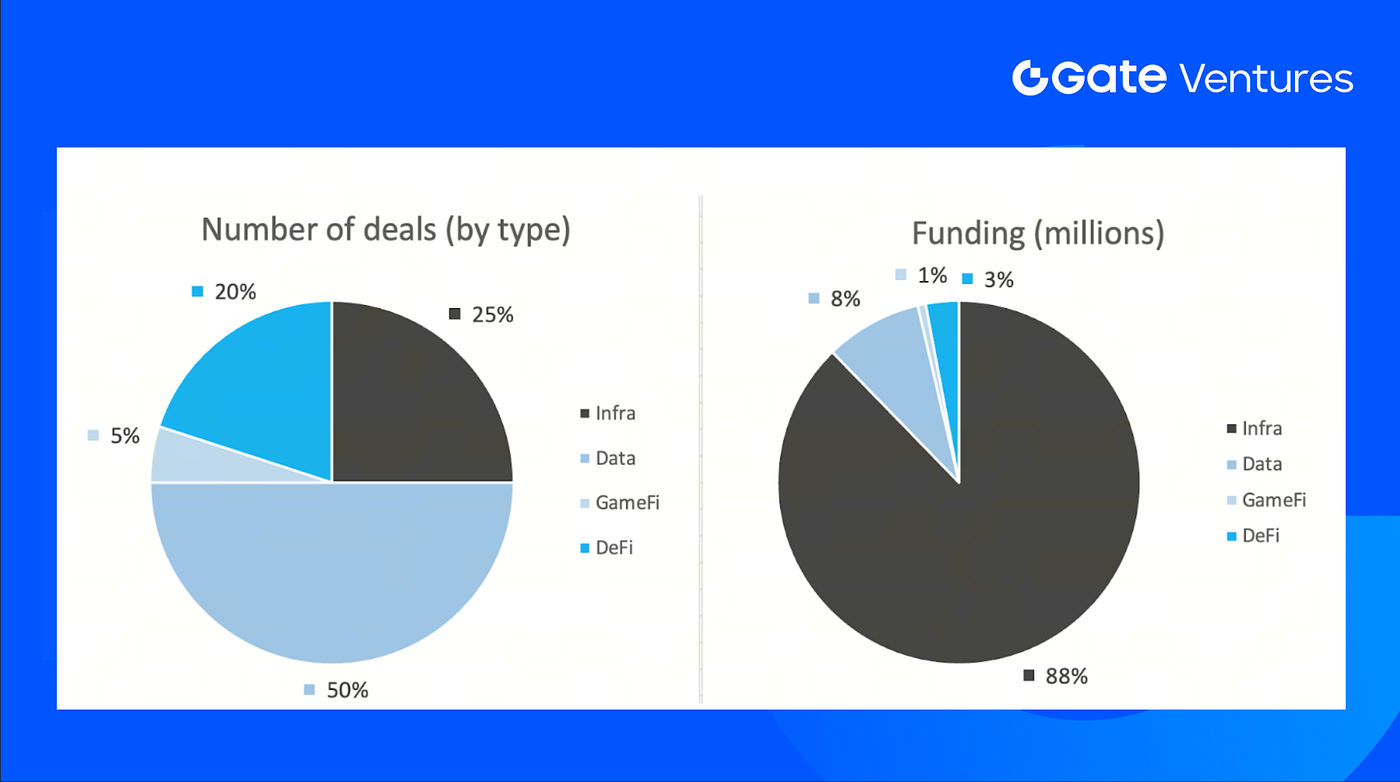

La semaine précédente, 20 deals ont été conclus : Data 10 (50 %), Infra 5 (25 %), GameFi 1 (5 %), DeFi 4 (20 %).

Récapitulatif hebdomadaire des deals Venture, Source : Cryptorank et Gate Ventures, au 24 novembre 2025

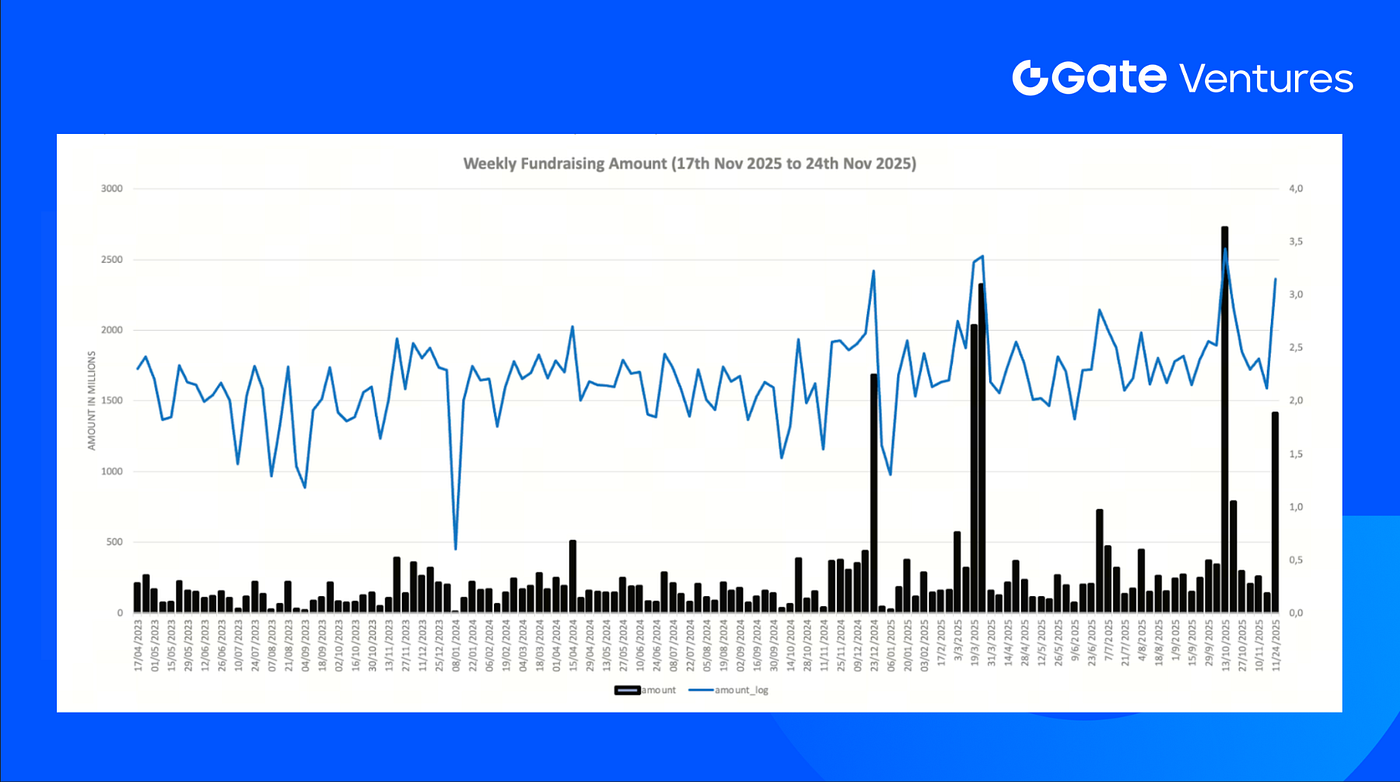

Le montant total des fonds levés annoncés la semaine précédente atteint 1 410 M$, 35 % (7/20) des deals n’ayant pas publié de montant. Le secteur Infra domine avec 1 237 M$. Les plus gros deals : Kalshi 1 000 M$, Kraken 200 M$.

Récapitulatif hebdomadaire des deals Venture, Source : Cryptorank et Gate Ventures, au 24 novembre 2025

La collecte hebdomadaire atteint 1 410 M$ pour la 3e semaine de novembre 2025, soit une augmentation de 968 % par rapport à la semaine précédente. Sur un an, la collecte progresse de 279 % sur la même période.

À propos de Gate Ventures

Gate Ventures, branche capital-risque de Gate.com, se concentre sur l’investissement dans l’infrastructure décentralisée, l’intergiciel et les applications qui façonneront l’ère Web 3.0. Aux côtés des acteurs majeurs du secteur, Gate Ventures accompagne des équipes et startups prometteuses dotées des idées et compétences pour redéfinir les interactions sociales et financières.

Site web | Twitter | Medium | LinkedIn

Ce contenu ne constitue ni offre, ni sollicitation, ni recommandation. Il est conseillé de solliciter un avis professionnel indépendant avant toute décision d’investissement. Gate Ventures peut restreindre ou interdire l’accès à tout ou partie de ses services dans certaines juridictions. Pour plus d’informations, veuillez consulter les conditions d’utilisation applicables.

Références :

- S&P Global Weekly Ahead Economic Data, https://www.spglobal.com/marketintelligence/en/mi/research-analysis/week-ahead-economic-preview-week-of-17-november-2025.html

- Fed Decision in December, Polymarket, https://polymarket.com/event/fed-decision-in-december?tid=1763953866107

- DXY Index, TradingView, https://www.tradingview.com/chart/z1UD772v/?symbol=TVC%3ADXY

- US 10 Year Bond Yield, TradingView, https://www.tradingview.com/chart/z1UD772v/?symbol=TVC%3AUS10Y

- Gold Price, TradingView, https://www.tradingview.com/chart/z1UD772v/?symbol=TVC%3AGOLD

- BTC & ETH ETF Inflow, https://sosovalue.com/tc/assets/etf/us-btc-spot

- BTC Greed and Fear Index, https://alternative.me/crypto/fear-and-greed-index/

- Micro Strategy’s exclusion from index, https://www.investing.com/news/analyst-ratings/microstrategy-stock-faces-index-exclusion-risk-jpmorgan-warns-93CH-4371553

- Hyperliquid whale’s position, https://hypurrscan.io/address/0x8d0e342e0524392d035fb37461c6f5813ff59244

- WLFI token burn, https://www.bitget.com/amp/news/detail/12560605074433

- Hyperliquid token unlock, https://www.odaily.news/en/post/5207726

- Ethereum Foundation unveils Interop Layer to solve L2 fragmentation and interoperability, https://www.theblock.co/post/379355/ethereum-foundation-interop-layer-l2-ecosystem-feel-like-one-chain

- Aave Labs introduces high-yield savings app with insured deposits rails and 12,000-bank support, https://www.theblock.co/post/379080/aave-labs-high-yield-savings-app-insurance-backed-protection-deposits-1-million

- Paxos launches USDG0 to bring regulated dollar liquidity across chains, https://cointelegraph.com/news/paxos-labs-announces-launch-of-new-stablecoin-usdgo

- 0xbow raises $3.5M Seed gound amid growing demand for regulated privacy rails, https://www.theblock.co/post/379395/0xbow-raises-3-5-million-seed-round-ethereum-foundation-backed-privacy-pools

- Former BlackRock team lands $4.6M for HelloTrade — mobile-first U.S. assets trading infrastructure, https://fortune.com/2025/11/20/former-blackrock-employees-raise-4-6-million/

- Ledn receives strategic investment from Tether to scale BTC-collateralized credit loan, https://tether.io/news/tether-makes-strategic-investment-in-ledn-expanding-opportunities-in-bitcoin-backed-lending/