شهدت أسواق المشتقات المالية على السلسلة تطورًا ملحوظًا، مما دفع منصات التداول اللامركزية إلى تجاوز حدود مبادلات الرموز البسيطة. مع تصاعد الطلب على الخيارات والعقود الدائمة والتداول بالرافعة المالية، أصبحت البروتوكولات على السلسلة تتبنى بشكل متزايد بنى تحتية مالية تقليدية، مثل دفاتر الطلبات ومحركات المخاطر وأنظمة الهامش.

في ساحة المشتقات على السلسلة، يُصنف Derive نفسه كمنصة تداول احترافية. مهمته الأساسية هي تقديم تجربة تداول تضاهي البورصات المركزية، ولكن ضمن بيئة حفظ ذاتي. ولتحقيق ذلك، يدمج Derive شبكة طبقة ثانية، ودفتر الطلبات المحددة المركزية (CLOB)، وهامش المحفظة، والتسوية على السلسلة لبناء بنية تحتية متكاملة تغطي مطابقة الطلبات وتقييم المخاطر وإدارة رأس المال.

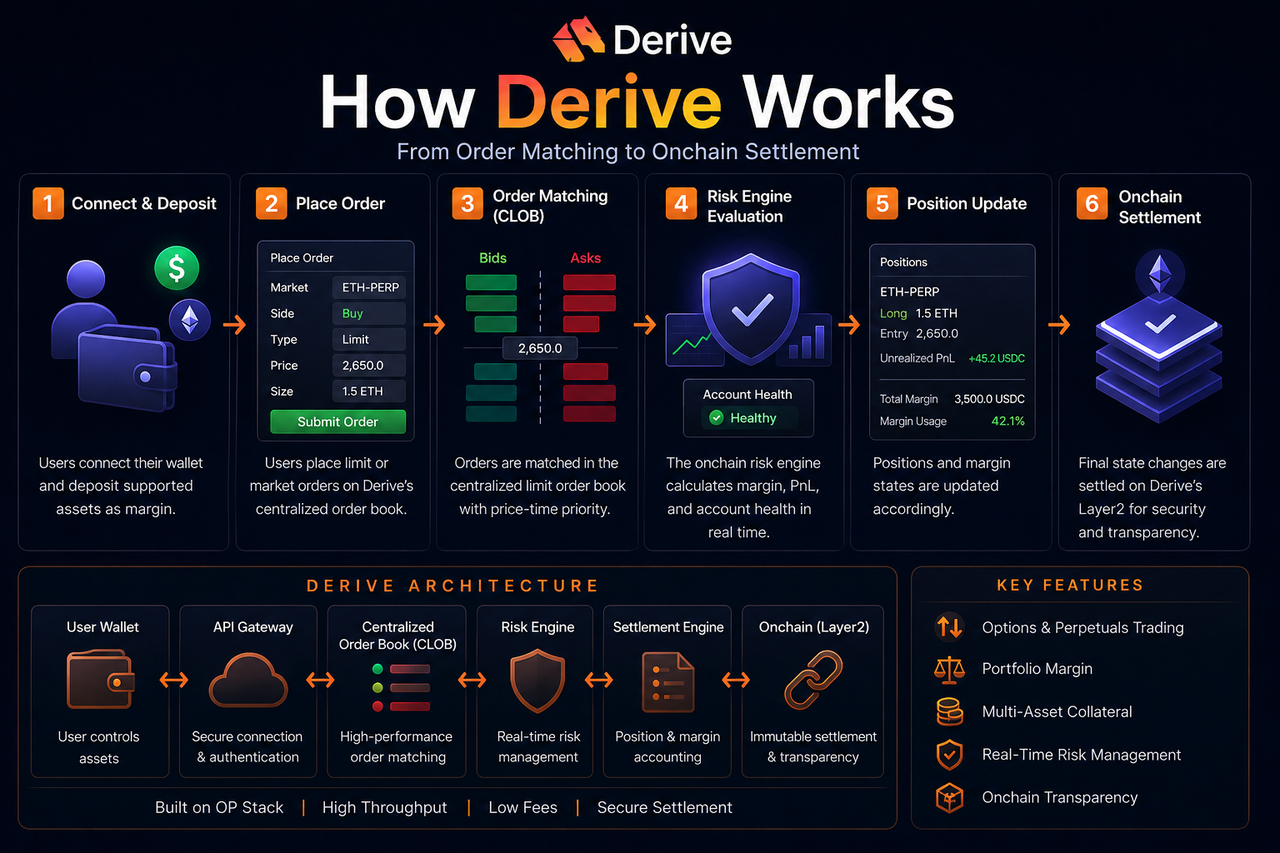

مكونات نظام تداول Derive

يتألف نظام تداول Derive من دفتر طلبات، ومحرك مخاطر، ونظام هامش، ووحدة تسوية، وشبكة طبقة ثانية. تعمل هذه المكونات معًا لتشكيل مسار تداول مشتقات كامل على السلسلة.

يدير دفتر الطلبات تقديم الطلبات ومطابقتها، ويقيّم محرك المخاطر حالة الحساب ومتطلبات الهامش بشكل مستمر، بينما يتولى نظام التسوية تحديث المراكز ونقل الأصول ومزامنة الحالة على السلسلة.

على عكس نماذج AMM التقليدية، يعتمد Derive هيكل سوق قائم على الطلبات. هذا النموذج مناسب بطبيعته لتداول المشتقات، إذ يتيح تسعيرًا أكثر دقة وإدارة سيولة بكفاءة أعلى.

الشبكة الأساسية لـ Derive مبنية على OP Stack، مما يمنح البروتوكول تكاليف رسوم أقل وإنتاجية معاملات أعلى في بيئة الطبقة الثانية.

كيفية بدء التداول على Derive

قبل التداول، يجب على المستخدمين إنشاء حساب وإيداع ضمان.

بصفته بروتوكول حفظ ذاتي، يتيح Derive للمستخدمين الاحتفاظ بالسيطرة على أصولهم عبر محافظهم على السلسلة. يقوم المستخدمون عادةً بإيداع عملات مستقرة أو ضمانات مدعومة أخرى في البروتوكول، لتصبح رصيد حساب الهامش الخاص بهم.

يدعم Derive ضمانات متعددة الأصول، مما يمنح المستخدمين مرونة في استخدام أكثر من عملة مستقرة واحدة كهامش. يحسب النظام قيمة الضمان والتعرض للمخاطر استنادًا إلى معايير المخاطر المحددة لكل أصل.

بعد إيداع الهامش، يمكن للمستخدمين تداول الخيارات أو العقود الدائمة عبر دفتر الطلبات. يتغير الهامش المتاح ديناميكيًا بتغير المراكز.

آلية مطابقة الطلبات في Derive

يستخدم Derive دفتر الطلبات المحددة المركزية (CLOB) لمطابقة الطلبات.

يمكن للمستخدمين تقديم طلبات محددة أو طلبات سوق. تدخل الطلبات إلى دفتر الطلبات وتُطابق حسب أولوية السعر والوقت. عندما يتطابق سعر البيع مع سعر الشراء، يُنفذ الطلب وتُحدث مراكز الطرفين.

يقدم نموذج دفتر الطلبات اكتشاف أسعار أكثر دقة مقارنة بـ AMMs، وهو أمر حيوي خاصة في أسواق الخيارات حيث تخلق أسعار التنفيذ المتنوعة وتواريخ انتهاء الصلاحية والتقلب هياكل تسعير معقدة. هذا يجعله مثاليًا لتداول المشتقات الاحترافي.

بالرغم من اعتماد Derive على محرك مطابقة عالي الأداء، فإن جميع حالات المراكز النهائية وتغيرات رأس المال تُزامن مع شبكة السلسلة، لضمان الشفافية وقابلية التحقق.

كيف يقيّم محرك مخاطر Derive مخاطر الحساب؟

محرك المخاطر هو أحد أهم وحدات Derive.

نظرًا لاحتمال امتلاك المستخدمين مراكز دائمة وخيارات متعددة في آن واحد، لا يمكن للنظام تقييم المخاطر بشكل منفرد. لذلك، يستخدم Derive هامش المحفظة لتقييم التعرض الصافي للمخاطر للحساب بأكمله.

فعلى سبيل المثال، إذا كان المستخدم يحمل مراكز شراء وبيع معًا، فإن بعض المخاطر تتعارض، مما يسمح للنظام بتقليل متطلبات الهامش الإجمالية. هذا يعزز كفاءة رأس المال مقارنة بنماذج الهامش المعزول.

يراقب محرك المخاطر عدة مقاييس في الوقت الفعلي:

| مؤشر المخاطر |

الوظيفة |

| أسهم الحساب |

قياس الحالة الإجمالية للأصول |

| الهامش الأولي |

الحد الأدنى لفتح مركز |

| هامش الصيانة |

الحد الأدنى لتجنب التصفية |

| معلمات التقلب |

ضبط أوزان المخاطر للأصول المختلفة |

| عمق السيولة |

تقييم مخاطر تأثير السوق |

يقوم النظام بتعديل معايير المخاطر ديناميكيًا بناءً على تقلبات السوق، مما يقلل المخاطر النظامية أثناء الأحداث القصوى.

متى يتم تفعيل آلية التصفية في Derive؟

تُفعّل التصفية عندما ينخفض هامش الحساب عن متطلبات هامش الصيانة.

صُمم نظام التصفية لمنع الحسابات من أن تصبح معسرة. إذا أدت تحركات الأسعار السريعة إلى توسيع الخسائر، يقوم النظام تلقائيًا بتقليل المراكز أو إغلاقها لإعادة الحساب إلى مستوى آمن.

في نموذج هامش المحفظة، يقيّم النظام مخاطر الحساب الإجمالية أولاً، دون تصفية المراكز بشكل منفرد. هذا يعني أن المراكز المحوّطة يمكن أن تقلل من احتمالية التصفية.

ومع ذلك، في الأسواق شديدة التقلب ومنخفضة السيولة، قد تزيد تكاليف الانزلاق السعري وخسائر التصفية. تظل إدارة المخاطر جزءًا لا يتجزأ من تداول المشتقات على السلسلة.

آلية معدل تمويل العقود الدائمة

العقود الدائمة لا تنتهي صلاحيتها، لذا تعمل آلية معدل التمويل على محاذاة سعر العقد مع السوق الفوري.

عندما يكون سعر العقد الدائم أعلى من السعر الفوري، يدفع أصحاب المراكز الطويلة معدل التمويل لأصحاب المراكز القصيرة عادةً، والعكس صحيح.

تحفز هذه الآلية المتداولين على تعديل مراكزهم، مما يقلل انحراف السعر.

على Derive، يتكيف معدل التمويل ديناميكيًا بناءً على العرض والطلب وهيكل المركز. غالبًا ما تؤدي الرافعة المالية العالية والظروف القصوى إلى ارتفاع حاد في معدل التمويل.

الفرق بين Derive والبورصات المركزية التقليدية في عملية التداول

تتمثل الفروق الرئيسية في حفظ الأصول والتسوية.

في البورصات المركزية، يُودع المستخدمون أصولهم في حسابات تسيطر عليها المنصة. على Derive، يحتفظ المستخدمون بالسيطرة عبر محافظهم على السلسلة، بينما يتولى البروتوكول التداول وإدارة المخاطر.

تستخدم البورصات المركزية مطابقة غير متصلة بالإنترنت وتحديثات قاعدة بيانات كاملة، بينما يحتاج Derive إلى مزامنة حالات التداول النهائية مع السلسلة، مما يتطلب موازنة بين الأداء واللامركزية.

من خلال بنية الطبقة الثانية ودفتر الطلبات عالي الأداء، قلّص Derive فجوة التجربة مع البورصات المركزية بشكل كبير.

مزايا Derive والقيود المحتملة

تكمن القوى الأساسية لـ Derive في كفاءة رأس المال العالية والتداول الاحترافي. يتيح هامش المحفظة والضمانات متعددة الأصول ونموذج دفتر الطلبات تنفيذ استراتيجيات معقدة.

تعمل شبكة الطبقة الثانية على تقليل تكاليف المعاملات وزيادة سرعة معالجة الطلبات، وهو أمر حيوي للمشتقات عالية التردد.

ولكن، تجلب هذه البنية تعقيدًا أكبر، حيث قد تكون الخيارات والهامش وإدارة المخاطر صعبة على المستخدمين العاديين.

بالإضافة إلى ذلك، تواجه البروتوكولات على السلسلة مخاطر العقود الذكية وعبر السلسلة والسيولة. قد يؤدي نقص عمق السوق إلى تدهور تجربة دفتر الطلبات.

الخاتمة

Derive هو بروتوكول تداول احترافي للمشتقات على السلسلة، يغطي مطابقة الطلبات وإدارة الهامش وتقييم المخاطر والتصفية والتسوية على السلسلة. من خلال توظيف شبكة الطبقة الثانية ودفتر الطلبات المحددة المركزية وهامش المحفظة، يهدف Derive إلى تقديم تجربة تداول في بيئة حفظ ذاتي تضاهي البورصات المهنية التقليدية.

الأسئلة الشائعة

ما هو هامش المحفظة في Derive؟

هامش المحفظة هو نظام يقيّم التعرض للمخاطر للحساب بأكمله، بدلاً من حساب الهامش لكل مركز على حدة.

لماذا يحتاج Derive إلى شبكة طبقة ثانية؟

تعمل الطبقة الثانية على خفض تكاليف الرسوم وزيادة سرعة المعاملات، مما يجعلها مثالية لتداول المشتقات عالي التردد.

كيف تعمل آلية التصفية في Derive؟

عندما ينخفض هامش الحساب عن متطلبات هامش الصيانة، يقوم النظام تلقائيًا بتقليل المراكز أو إغلاقها للحد من المخاطر الإجمالية.

ما وظيفة معدل تمويل العقود الدائمة؟

يحافظ معدل التمويل على محاذاة سعر العقد الدائم مع السعر الفوري.

ما الفرق بين Derive والبورصات المركزية؟

يُولي Derive الأولوية للحفظ الذاتي وشفافية التسوية على السلسلة، بينما تعتمد البورصات المركزية عادةً على نموذج حفظ من قبل المنصة.