Futures

Access hundreds of perpetual contracts

TradFi

Gold

One platform for global traditional assets

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Introduction to Futures Trading

Learn the basics of futures trading

Futures Events

Join events to earn rewards

Demo Trading

Use virtual funds to practice risk-free trading

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

Trade on-chain assets and earn airdrops

Futures Points

Earn futures points and claim airdrop rewards

More

Pig prices hit a six-year low, Muyuan Foods' revenue is expected to grow by 4.5% in 2025, with net profit down 16.5%, and the slaughtering business turning a profit for the first time.

The downward cycle of pig prices has put pressure on China’s largest hog farming company, but cost control and a transformation in the slaughtering business have built new profit support for it.

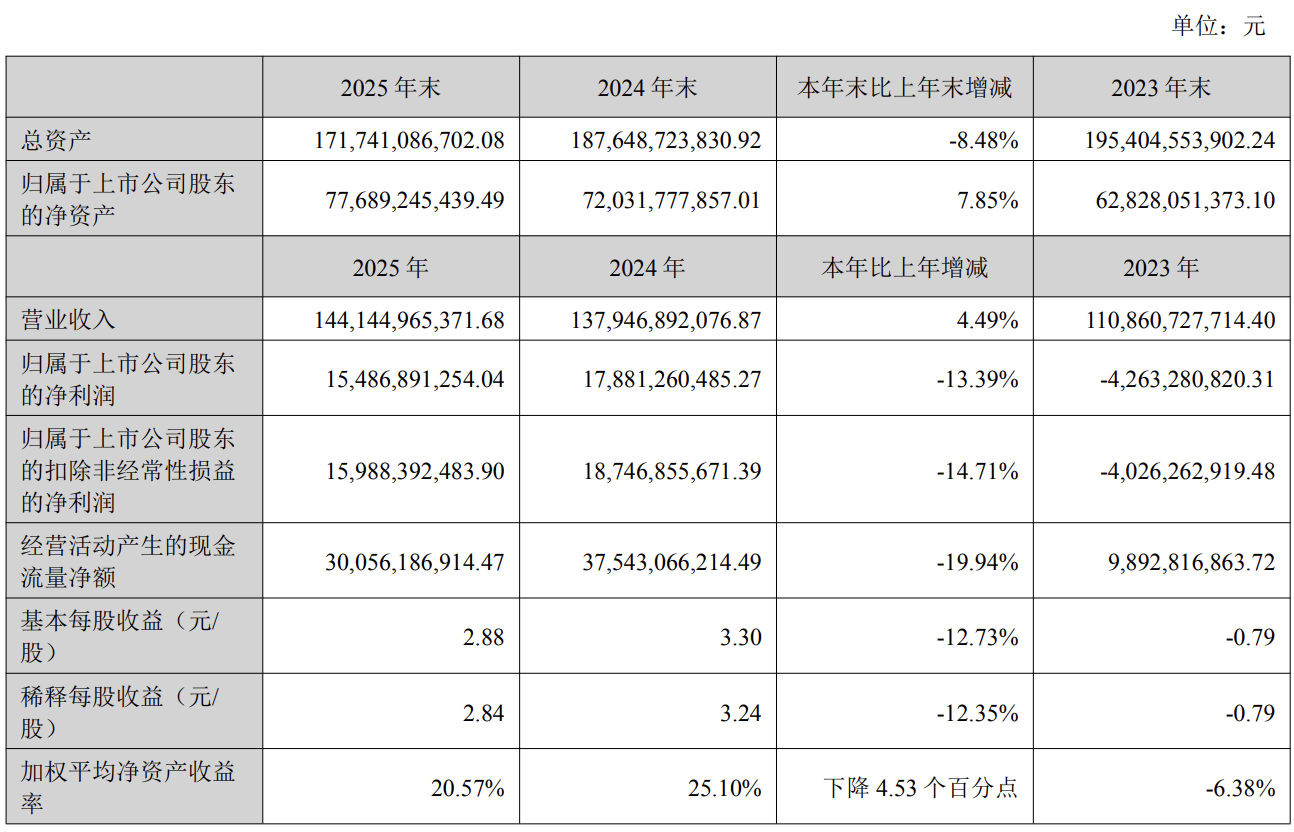

Mudanjiang Food Co., Ltd. reported in its 2025 annual report that the company achieved operating income of 144.145 billion yuan, a year-on-year increase of 4.49%; the net profit attributable to shareholders was 15.487 billion yuan, a year-on-year decrease of 13.39%. The company attributed the decline in profits primarily to the year-on-year drop in pig prices, with the average price of live pigs for the entire year of 2025 falling to 14.44 yuan/kg, the lowest since 2019.

It is worth noting that the company’s total cost of hog farming for the entire year of 2025 dropped to about 12 yuan/kg, a decrease of about 2 yuan/kg compared to the same period last year, which to some extent offset the impact of falling pig prices.

Meanwhile, the operating income from the slaughtering and meat business surged by 86.32% year-on-year, achieving annual profitability for the first time in 2025, becoming an important new highlight in the company’s performance structure. The company also announced a cash dividend of 4.27 yuan for every 10 shares, with a total dividend amount of about 2.435 billion yuan.

Low Pig Prices Weigh on Profits, Cost Improvements Create Hedge

In 2025, the supply of live pigs in the market continued to expand. According to data from the National Bureau of Statistics, the national pig slaughter volume reached 71.973 million heads, a year-on-year increase of 2.4%, and the pork output hit a historical high of 5.938 million tons.

The oversupply has depressed prices, with the average price of live pigs for the year dropping by 9.2% year-on-year, showing a “high in the front and low in the back, fluctuating downward” pattern. It is estimated that the average profit per head of live pigs for the entire industry was 31 yuan, a decrease of 183 yuan compared to 2024.

Facing industry headwinds, Mudanjiang achieved significant cost reductions through technological innovation and optimization of production management. The total cost for 2025 was about 12 yuan/kg, a year-on-year decrease of about 2 yuan/kg, with declining prices for feed raw materials such as corn and soybean meal also contributing—feed costs account for about 55% to 65% of the total cost of hog farming.

From a financial perspective, the net profit attributable to shareholders of the listed company, excluding non-recurring gains and losses, was 15.988 billion yuan, a year-on-year decrease of 14.71%; basic earnings per share were 2.88 yuan, a year-on-year decrease of 12.73%.

Slaughtering Business Achieves Annual Profit for the First Time, Becoming a New Profit Growth Engine

Mudanjiang’s slaughtering and meat segment achieved operating income of 45.228 billion yuan in 2025, a year-on-year increase of 86.32%, and for the first time realized annual profitability, with an annual capacity utilization rate reaching 98.8%. Profits were achieved in both the third and fourth quarters.

By the end of 2025, the company had established over 70 sales branches in 20 provincial-level administrative regions nationwide for its slaughtering and meat business, slaughtering 28.663 million pigs and selling 3.23 million tons of fresh and frozen pork products throughout the year.

The company is also gradually deepening its product structure by cultivating higher-quality pork varieties through breeding technology, and performing more refined cuts of pork products to cover different consumer tier demands. The slaughtering end directly obtains consumer demand information, forming a linkage with the farming end, injecting new synergistic value into the company’s vertical integration model.

Financial Structure Continues to Optimize, Increased Shareholder Returns

On the liability side, Mudanjiang’s total liabilities at the end of 2025 decreased by 17.1 billion yuan compared to the beginning of the year, with the debt-to-asset ratio dropping from 58.68% to 54.15%, a decrease of 4.53 percentage points; total assets amounted to 171.741 billion yuan, a year-on-year decrease of 8.48%.

The net cash flow generated from operating activities was 30.056 billion yuan, down from 37.543 billion yuan the previous year. In terms of bond ratings, China Chengxin International maintained the company’s issuer and “Mudanjiang Convertible Bonds” rating at AA+ in May 2025, with a stable rating outlook.

In terms of shareholder returns, the company implemented two equity distributions during the reporting period, totaling 8.085 billion yuan in dividends and completed a share repurchase of about 2 billion yuan. The profit distribution plan disclosed in this annual report for 2025 is a cash dividend of 4.27 yuan for every 10 shares (including tax), with a total dividend amount of about 2.435 billion yuan.

The company also established a “Market Value Management System” during the same period and completed its listing on the Hong Kong Stock Exchange in February 2026, aiming to attract more international and long-term investors and optimize the shareholder structure.

Capacity Control Tightens, Industry Supply and Demand Expected to Gradually Improve

Supply-side policies continue to tighten. The Ministry of Agriculture and Rural Affairs in 2024 lowered the target for the normal breeding sow inventory from 41 million heads to 39 million heads, and since 2025, the language for capacity control has been further strengthened, deploying multiple measures to reduce the breeding sow inventory, control slaughtering weight, and strictly control new capacity.

Due to this guidance, combined with market self-regulation, the inventory of breeding sows accelerated to decrease in the second half of 2025, falling to 39.61 million heads by the end of December, down 1.16 million heads year-on-year, a decrease of 2.9%, approximately 101.6% of the normal inventory.

The degree of industry scale has also improved. According to monitoring data from the Ministry of Agriculture and Rural Affairs, the scale rate of hog farming is expected to reach about 73% in 2025. Mudanjiang is also accelerating its international layout in this context, having established a subsidiary in Vietnam and signed a cooperation agreement with Vietnam’s BAF Company to explore expanding overseas markets through equipment and technology.

Risk Warning and Disclaimer