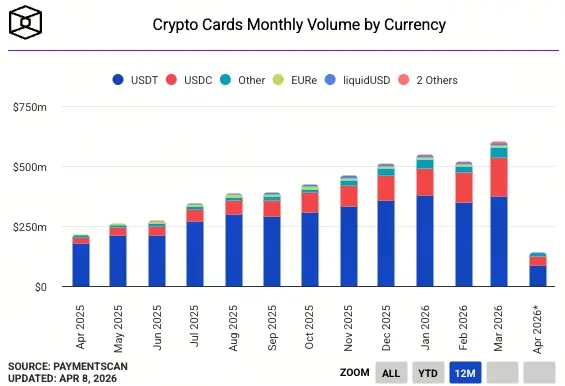

Based on the latest data, in March the monthly transaction volume of crypto cards (including debit cards and prepaid cards) reached $600 million, up more than threefold from $187 million in the same period last year—reflecting that the global adoption of crypto cards as a digital-asset payment tool continues to accelerate. The market share of USDT, which has long dominated crypto card settlements, is gradually shrinking; USDC’s share continues to rise, indicating a structural shift in the geographic distribution and user composition of stablecoins in the payments space.

Triple the transaction volume growth: Why crypto cards have become a new everyday payments tool

The core competitive advantage of crypto cards lies in significantly reducing the friction cost for native on-chain users to enter everyday consumer scenarios. Traditional exit routes for crypto assets involve multiple intermediate steps—selling assets on an exchange, waiting for funds to arrive, and then spending with fiat currency—making the process cumbersome. Crypto cards allow users to spend directly at the point of sale (POS) with stablecoins such as USDT or USDC, without needing to rely on traditional payment infrastructure, fundamentally simplifying the path to use.

This trend is especially pronounced in emerging markets. In regions like Southeast Asia, Latin America, and Africa, where traditional banking services are less widespread, crypto cards have become a more practical alternative payment solution rather than a niche tool within the crypto community.

USDT vs. USDC market share shifts: Geography determines the landscape

Geographic distribution characteristics of settlement currencies for crypto cards

USDT-dominant regions: Emerging markets such as Southeast Asia, Latin America, and Africa. In areas where traditional banking services are inadequate, USDT has long held the lead thanks to its broad circulation base and high liquidity, and is viewed as a stored-value and payment tool that replaces fiat

USDC growth regions: Western markets such as North America and Europe. Higher regulatory transparency and strong institutional backing give USDC a clear advantage among compliant-focused issuers and users

Trend direction: USDT’s market share in crypto card transaction volume is gradually shrinking, USDC continues to rise, and the user base has clearly expanded beyond Tether’s traditional stronghold

Changes in stablecoins’ share of transaction volume for crypto cards are considered an important indicator for tracking the evolution of digital payments geography and demographics, and can effectively reflect who is using these products, where they use them, and how differences in regulatory requirements vary across markets.

Tether’s strategic response: The competitive implications of a U.S. stablecoin plan

In response to USDC’s rapid expansion in Western markets, Tether has said it intends to launch a dedicated, compliant stablecoin product for the U.S. market. If Tether’s U.S. version successfully gains regulatory approval, it could slow down—or even reverse—the growth of USDC’s market share in the U.S., which is the most notably expanding region for USDC in recent years.

This strategic move will become a key variable to watch in the evolution of the settlement-currency landscape for crypto cards. The market is assessing whether Tether’s compliant U.S. product can effectively compete with the Western user base that USDC has deeply penetrated.

Frequently asked questions

Why has crypto card transaction volume grown more than threefold in just one year?

Crypto cards eliminate the cumbersome processes of traditional crypto-asset exit routes, allowing users to spend directly with USDT or USDC at the point of sale without first converting to fiat. Demand in emerging markets for alternatives to traditional banking, along with improvements to compliance-focused infrastructure in Western markets, jointly drive rapid growth in user scale. Monthly transaction volume increased from $187 million to $600 million.

Why is USDC’s share of crypto card transactions continuing to rise?

USDC is issued by Circle and is known for regulatory transparency and institutional backing, giving it a clear competitive advantage in North American and European markets that prioritize compliance. As the crypto card user base expands from emerging markets to Western markets, USDC’s market share continues to rise, gradually narrowing the gap with USDT.

Will Tether’s launch of a U.S. stablecoin threaten USDC’s market position?

Tether has confirmed its intention to launch a compliant stablecoin product for the U.S. market. If it successfully rolls out, it could form direct competition in regions where USDC is expanding the fastest. However, USDC has already built a relatively deep institutional partnership network in the U.S. The market influence of a new entrant still depends on how the regulatory environment evolves and how readily the market actually accepts the product.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.